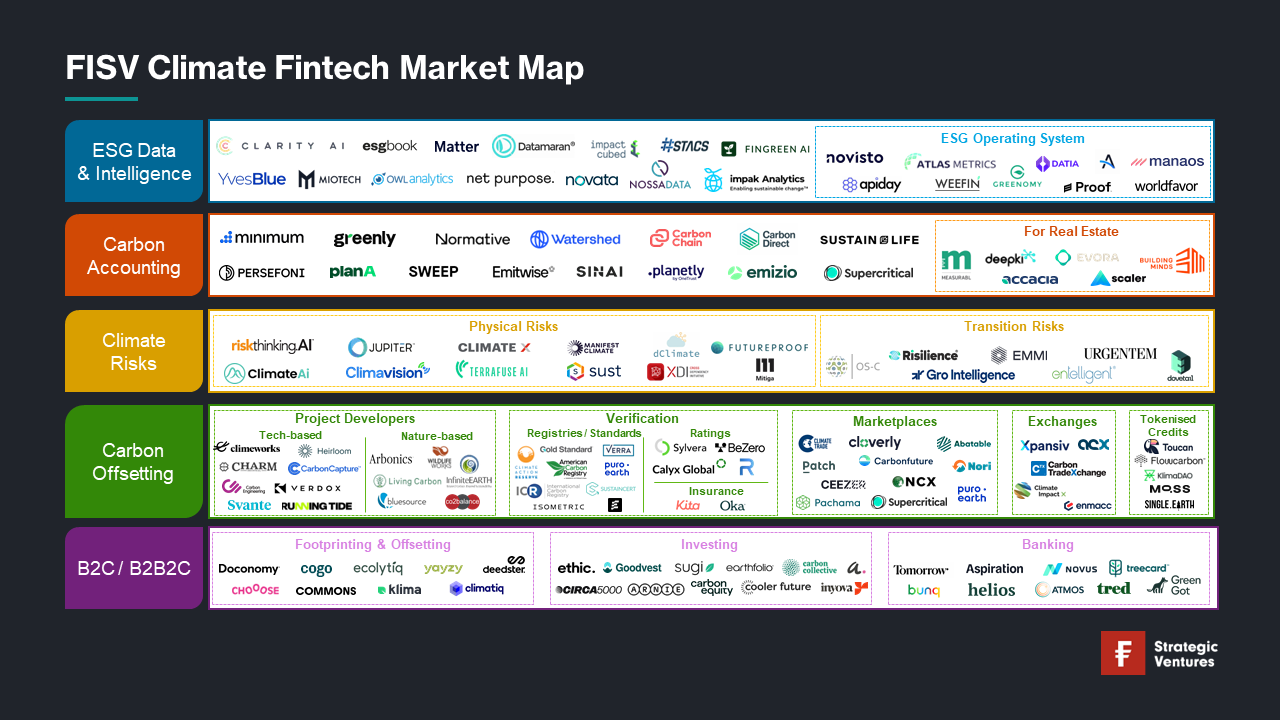

Diving into the Climate Fintech Landscape

The emergence of fintech companies focusing on innovative climate solutions has gained significant momentum in recent years. They are offering fresh perspectives to financial institutions and corporations, helping them achieve their climate goals. As world leaders begin to grasp the urgency of the situation, climate technology is rapidly maturing beyond just being a hot topic. The rising public interest in sustainability is also driving the introduction of regulations aimed at holding corporations accountable and eradicating greenwashing. This shift in the market has fuelled a spike in climate fintech deals, with over $6 billion transacted since 2020.

Over the past three years, we’ve been monitoring and exploring this rapidly growing space, with a particular focus on B2B players serving the needs of asset managers and other large financial institutions. Below, we share some of our current thinking as we continue to track and explore exciting opportunities across this dynamic landscape.

-

Bridging the Climate Data Gaps

Quality data, or the lack thereof, remains the primary ESG challenge facing financial institutions and investors. Despite growing interest in sustainable investments, many portfolio assets still lack comprehensive climate-related information. While listed equities and bonds have a fair share of coverage, other asset classes fall short. Private markets, for instance, offer limited climate disclosures. But change is on the horizon, with firms like Novata and esg.book targeting this particular asset class and aiming to close that data gap.

As we transition from a scarcity to an abundance of ESG data, we face the next challenge: standardising data. Although a single set of reporting standards won’t solve all problems, standardisation can enhance reporting efficiency and data comparability. Such uniformity will facilitate assessing, validating, and comparing company progress across these critical issues and improve investor confidence. We anticipate a standardisation in sustainability reporting similar to the convergence of accounting standards like IFRS and US GAAP, the premises of which we're already witnessing. The implementation timeline remains uncertain, but our prediction falls within the next three to five years.

-

Addressing Data Integration Challenges

Despite improvements in ESG datasets, a ‘one-stop shop’ does not exist yet. Financial institutions find themselves juggling data from multiple vendors to form a clear picture of a company's sustainability performance. This data must then be integrated into their internal systems and technology stack, which is often a complex and time-consuming process. Fintechs like Novisto or Weefin, however, are addressing this issue by developing data operations platforms. Their solutions allow companies to house all their ESG data in one place, promoting consistency and enabling collaboration, ultimately driving superior decision-making and value creation.

-

Streamlining Carbon Management

We’ve noticed a surge in carbon accounting start-ups offering intuitive software to help companies measure, reduce, and offset their carbon footprint. There’s a clear need for these tools, as many organisations still rely on Excel spreadsheets or consultancy services (for the large and complex ones) to calculate their emissions, a process that is inefficient, costly, and non-repeatable. Notably, the space is very well-funded but crowded; we foresee consolidation and predict success for those with robust data capabilities, flexible technology, and value-add services like Greenly and Plan A.

-

Assessing and Pricing Climate Risks

Climate change is no longer a distant reality; its effects are here, triggering extreme weather events and causing substantial financial losses. This is a challenging era for financial institutions, especially when these one-off events have turned into recurring episodes. Investment managers face the daunting task of integrating climate change projections to assess risk and return expectations that inform security selection in investment portfolios. However, the lack of quality and complete datasets challenges their ability to do this effectively. A few companies are tackling this space, including Jupiter Intelligence and Riskthinking.AI in physical risks and Risilience in transition risks. At a time when increasing climate volatility is putting trillions of dollars of assets at risk, financial institutions require robust climate intelligence to help them form sound investment decisions

-

Carbon: A New Asset Class

Decarbonisation is the critical first step towards achieving net zero. The world largely concurs on the need to hit net-zero emissions by 2050, but less than 60% of companies are on track to meet this target. Achieving a zero-carbon economy will require a colossal capital investment of $3.5 trillion annually over the next three decades. This includes initiatives to cut carbon emissions and investments in carbon credits to offset unavoidable emissions. We are falling behind in action and investment, and a data deficit makes it hard to measure progress against net-zero targets and gauge the impact of climate investments.

To help bridge this gap, we recently invested in Sylvera's Series B, a leading provider of carbon data. Their trusted and unconflicted data is helping asset managers evaluate the net-zero plans of investee companies globally. It also facilitates the development of new sustainable investment products (e.g., sustainability-linked bonds), educates investors about the quality of carbon offsets, and helps avoid greenwashing. This is a major stride towards institutionalising carbon markets, which will assist corporations and investors in attaining their net-zero ambitions.

We are very excited about this space and are always looking to learn more. Feel free to reach out if you believe we'd be interested in your company or if you'd like to explore opportunities together: marine.auge@fisv.com

Note: The opinions expressed in this article are solely the author’s and do not necessarily reflect the views of Fidelity International.